TSP Rollover and Investment Strategy: Transfer Thrift Savings Plan to IRA or Roth IRA

An investment strategy in retirement is imperative for federal retirees because it helps ensure that your savings last throughout your retirement years while balancing growth, income, and risk management. Without a plan, retirees risk running out of money too soon or missing opportunities to maximize their wealth. Some common strategies include the bucket approach, which divides savings into short-term, medium-term, and long-term investments, and systematic withdrawals, such as the 4% rule, which adjusts withdrawals based on inflation and market performance.

Need help with the TSP Rollover Process? Meet with a Chartered Federal Employee Benefits Consultant (ChFEBC℠) today!

Why Most Federal Employees Roll Over Money from TSP to a Roth IRA or Traditional IRA Options.

The reason many federal retirees might want to move their TSP savings to an Individual Retirement Account (IRA), because doing so allows for greater flexibility and control over their investments. While the TSP offers low-cost funds, it has limited investment options compared to IRAs, which allow access to a broader range of assets. Additionally, transferring to an IRA can provide more tailored withdrawal strategies, tax planning opportunities, and estate planning benefits. However, retirees should be mindful of withdrawal rules—moving funds to an IRA may subject them to penalties if withdrawn before age 59½, whereas the TSP allows penalty-free withdrawals starting at age 55 for those who retire at that age or older.

TSP Investment Strategies for Federal Employees and Retirees

Investing in the Thrift Savings Plan (TSP) requires a well-thought-out strategy to balance growth and risk, especially as retirement approaches. Here’s a breakdown of key considerations:

1. Problems with Being Too Aggressive

While aggressive investing can lead to higher returns, it also comes with increased volatility. If a retiree or near-retiree has too much exposure to high-risk funds (like the C, S, and I Funds), they may experience significant losses during market downturns. This can be problematic if they need to withdraw funds during a market dip, locking in losses instead of allowing time for recovery. In retirement especially, whether you keep money in the TSP plan or move money from a Thrift Savings account to a pre-tax IRA or to Roth IRA plans, being too aggressive or too conservative for the withdrawal's time horizon can be detrimental to attaining one's retirement goals.

2. Importance of Time Horizons and Risk Tolerance

- Time Horizon: The longer you have until retirement, the more risk you can afford to take, as you have time to recover from market fluctuations. Younger investors can generally allocate more to stock-based funds, while retirees should shift toward more stable investments.

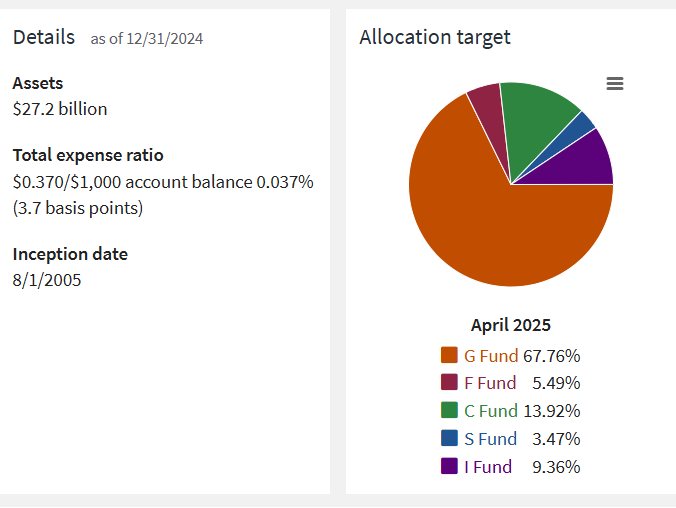

- Risk Tolerance: This is a highly personal definition. Some investors can handle market swings without stress, while others prefer stability. The L Funds (Lifecycle Funds) automatically adjust allocations based on retirement timelines, gradually shifting toward safer investments as retirement nears. Although, lifecycle funds are often chosen as a “set it and forget” strategy. This type of thinking can become problematic as retirement nears. As you can see below, we have included the allocation for the L Income fund, which each lifecycle fund eventually ends based on the target date chosen. The L Income fund becomes very G fund heavy and may leave your retirement nest egg falling short of inflation in the long-term.

Check out this article about moving money from a traditional TSP into an IRA

3. Need for Proper Portfolio Rebalancing

Rebalancing ensures that your portfolio maintains its intended risk level. Over time, some funds may grow faster than others, causing an imbalance. For example, if stock funds outperform, your portfolio may become riskier than intended. Rebalancing involves:

- Reviewing allocations every 6-12 months.

- Adjusting contributions or transfers to realign with your target percentages.

- Avoiding emotional decisions based on short-term market trends.

Would you like help determining an optimal TSP allocation based on your retirement goals? Schedule a meeting with a PlanWell Financial Advisor.

How to Roll Your TSP Account Money to a Traditional IRA or Roth IRA

Retirement Plan for Federal Workers: Steps to Complete a TSP to IRA Rollover

Rolling over a thrift savings plan to an IRA involves several key steps. First, you must instruct the TSP administrator to initiate the rollover process, specifying whether you want a direct or indirect rollover. A direct rollover is generally preferred, as it minimizes tax complications and ensures a seamless transfer of funds. Next, you need to establish a new IRA account if you don't already have one. Need a new IRA provider? Learn what makes PlanWell Financial different from other investment firms. Once the TSP funds are transferred, you can begin investing according to your retirement strategy. It's important to keep detailed records of the rollover to ensure compliance with IRS regulations and avoid any potential tax penalty.

Direct vs. Indirect Rollover of Funds from a TSP Account

Choosing between a direct and indirect rollover depends on your financial situation and preferences. A direct rollover involves transferring funds directly from the TSP to the IRA, eliminating the risk of withholding taxes and penalties. This method is generally recommended for its simplicity and tax efficiency. In contrast, an indirect rollover involves receiving the funds personally before depositing them into the IRA. While this option provides temporary access to the funds, it requires careful management to avoid tax consequences and ensure the rollover is completed within the 60-day window. Evaluating your needs and consulting with a financial advisor for federal employees can help determine the best approach for your rollover.

Common Mistakes to Avoid When You Roll Money from TSP to Traditional IRAs

When rolling over your TSP to an IRA, it's essential to avoid common pitfalls that can lead to costly mistakes. One common error is failing to complete the rollover within the required 60-day period, resulting in taxes and penalties. Additionally, neglecting to consider the tax implications of converting traditional TSP funds into a Roth IRA can lead to unexpected tax liabilities. It's also important to ensure that the rollover is executed correctly, with all necessary documentation and instructions provided to the plan administrator. 20% federal tax withholding must be selected and paid with non-retirement money (cash out of pocket), which is often what makes indirect rollovers so tricky. Seeking guidance from a financial advisor can help navigate these challenges and ensure a smooth transition.

Estimate your Retirement Income with the TSP Calculator Tool.

Why Consider a Rollover from TSP to an IRA?

Potential Tax Implications of a TSP Rollover

When considering a rollover from a TSP to an IRA, it's crucial to understand the potential tax implications. A direct rollover, where the TSP funds are transferred directly to the IRA, typically avoids immediate taxation. However, if you opt for an indirect rollover, where the funds are distributed to you before being deposited into the IRA, you may face withholding taxes and potential penalties if not completed within 60 days. Additionally, rolling over to a Roth IRA involves converting pre-tax TSP funds into a Roth account, which may trigger a taxable event. Knowing what type of IRA you are rolling into, and what source you're moving money from (pre-tax account or Roth TSP), is critical when entering the rollover amount. Account details can be found by logging into your TSP online portal.

TSP Plan Rollover Impact on Your Retirement Savings

A TSP rollover can significantly impact your retirement savings strategy. By moving money from your TSP to a traditional IRA, you gain greater control over your investment choices and potentially enhance your portfolio's growth potential. However, it's essential to consider the timing of the rollover, as market conditions and tax implications can affect the overall outcome. Additionally, understanding RMD rules and early withdrawal penalties is crucial to avoid unintended consequences. A well-planned rollover can optimize your retirement funds and align them with your long-term financial objectives.

TSP Planner: Items to Consider Before Making a TSP Withdrawal

Understanding the Basics of a TSP Account

The Thrift Savings Plan (TSP) is a retirement savings and investment plan specifically designed for federal employees and members of the uniformed services. As an employer-sponsored retirement plan, the TSP offers participants the opportunity to save for retirement through contributions that can be either pre-tax or post-tax, depending on whether you choose a traditional TSP or a Roth TSP. The plan administrator manages the TSP, providing a range of investment options that include government securities, fixed income, and stock index funds. The TSP account is similar to a 401k, allowing federal employees to accumulate retirement savings over time. While the TSP is great while employed, things can drastically change in retirement, meaning you will want to explore options for moving money from your Thrift Savings Plan account to a new account managed by a financial planner federal employees can trust.

Benefits of a TSP for Federal Employees

Federal employees benefit from the TSP's unique features, including the ability to make both traditional and Roth contributions. The traditional TSP allows for pre-tax contributions, reducing taxable income in the year of contribution, while the Roth TSP enables after-tax contributions, allowing for tax-free withdrawals in retirement. The TSP's low fees and government matching contributions further enhance its appeal, making it a valuable component of a comprehensive retirement plan. Additionally, the TSP's simplicity and automatic payroll deductions make it an accessible and efficient way for federal employees to save for retirement. That being said, there remain some problems with TSPthat should definitely be reviewed when developing your federal retirement plan.

Consulting a Financial Advisor for TSP Decisions

Given the complexities of TSP rollovers and withdrawals, consulting a financial advisor can be invaluable in making informed decisions. A financial advisor can provide personalized guidance on the best strategies for rolling over your TSP to an IRA or Roth IRA, considering your unique financial situation and retirement goals. They can also help navigate the tax implications and ensure compliance with IRS regulations. By working with a financial advisor, you can optimize your retirement savings and develop a comprehensive plan that aligns with your long-term objectives.

Learn More about the Fed-Expert Financial Advisors at PlanWell.