Have you retired or recently left Federal service? If so, you are probably wondering what you should do about the TSP. Should you leave your retirement funds with the Thrift Savings Plan (TSP) or transfer into a Individual Retirement Account (IRA)? It is an important question to ask.

What does TSP do well?

Some of the advantages of TSP are also disadvantages so continue reading until the end to find out why.

- Simple and easy to use

- The investment options are simple and straightforward. There are 5 “core” funds along with the lifecycle funds to choose from (excluding the mutual fund window). If you stay with TSP, you also do not need to spend time researching other financial institutions and individual investments.

- Low cost

- The average expense ratio for the “core” and lifecycle funds is around 0.07%. That’s about as low as it gets.

- G fund

- The G fund is unique only to TSP and is guaranteed by the US Government. As far as our understanding, you are unable to find a similar investment out there. The G fund’s investment objective is stated as follows: “to ensure preservation of capital and generate returns above those of short-term U.S. Treasury securities.” For additional background, you may find our history of the G Fund and TSP G Fund rate today informative.

- Mutual fund window

- The introduction of the mutual fund window now provides Federal employees the ability to choose from over 4,000 mutual funds. For an in-depth look, check out our Inside Look at the TSP Mutual Fund Window.

- Required Minimum Distributions (RMDs) are automatic

- TSP will automatically calculate and disburse your RMDs each year they are due. The auto payment is a great benefit to help prevent the high penalties that are accompanied if you miss an RMD.

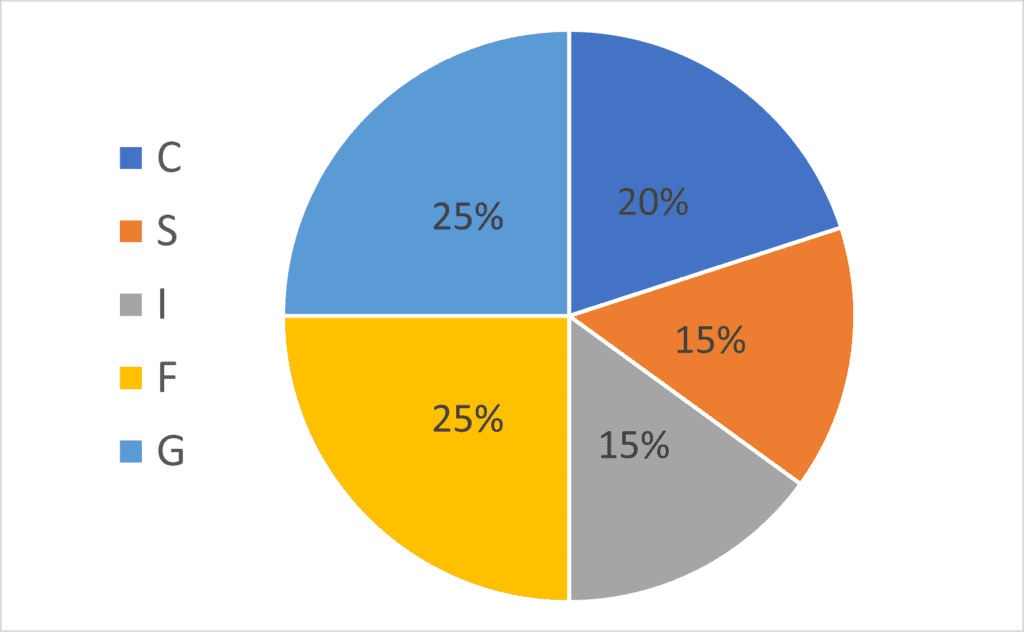

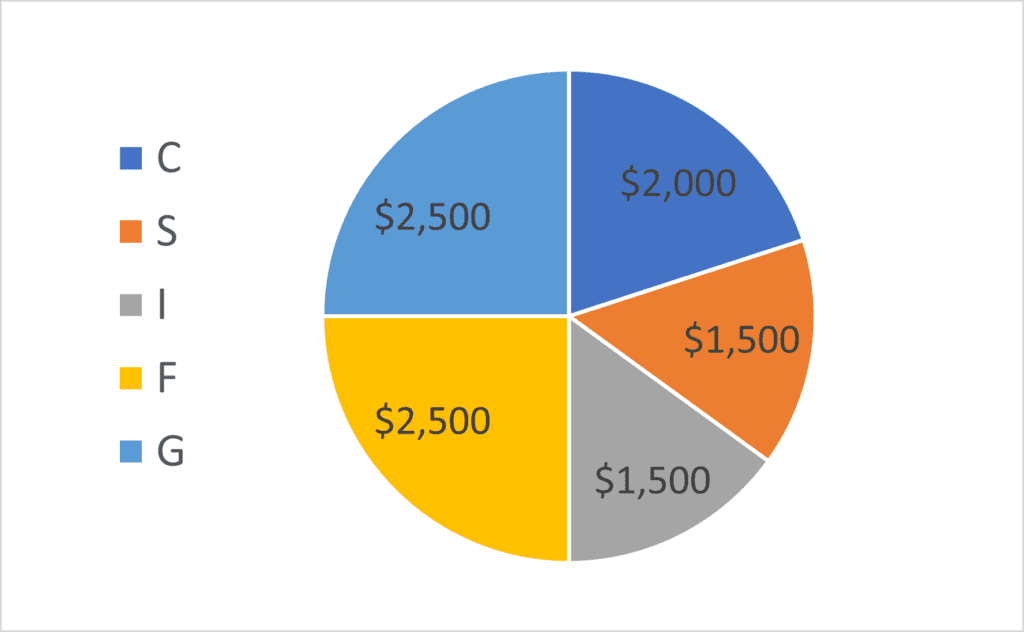

- Lifecycle funds

- The lifecycle funds are often chosen as a “set it and forget” strategy. This type of thinking can become problematic as retirement nears. As you can see below, we have included the allocation for the L Income fund, which each lifecycle fund eventually ends based on the target date chosen. The L Income fund becomes very G fund heavy and may leave your retirement nest egg falling short of inflation in the long-term.

- No guidance and limited customer support

- You are on your own. TSP is unable to give guidance on your account in regards to distributions, taxes, and investment strategy.

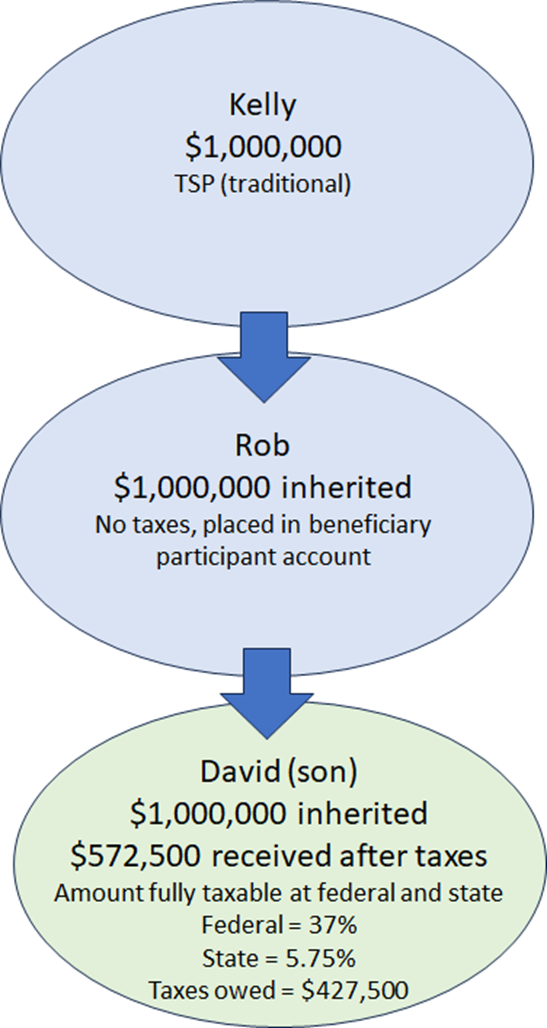

- Beneficiary designations and inheritance process

- There are no issues if a spouse receives the TSP if you predecease him/her, but what happens when a beneficiary participant dies? The money cannot remain in the Thrift Savings Plan. The payments must be made DIRECTLY to whom the beneficiary participant has chosen. That means, the money cannot be rolled over into a beneficiary IRA. This could result in a major tax liability for the beneficiary of a beneficiary participant.

- For example, say you predecease your spouse. Your spouse receives the TSP funds into a beneficiary participant account. When your spouse passes away, the funds go to your son or daughter. In this scenario, the full amount received will be TAXABLE. This is a huge problem. The children will be unable to place these funds into an inherited IRA and could possibly be taxed at the highest tax bracket.

Summary

When you retire or leave Federal service, it is important to consider all the options available. It can be comfortable to keep the status quo, but we would urge taking the time to do the research. You have saved an entire career to get where you are now. Don’t make an uninformed decision on a big part of your financial plan. If you are considering moving out of TSP, you may find our guide on whether you should transfer out of Thrift Savings Plan (TSP) helpful.

Reach Out to Us!

If you have additional federal benefit questions, contact our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciaries (AIF®). At PlanWell, we focus on retirement planning for federal employees, serving as a financial advisor for federal employees. Learn more about our process designed for the career federal employee.

Preparing for federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars in our workshop page. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out, and we’ll collaborate with HR to arrange an on-site FERS seminar.

Roth conversions can become an impactful tool at retirement. If you’d like to learn more, see our guide on Roth conversions. Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting using our contact page.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.