Avoid These Common TSP Misconceptions & Mistakes

The Thrift Savings Plan (TSP) is a critical component of federal employees’ retirement strategies, yet it’s shrouded in misconceptions and misunderstandings that can derail even the most meticulously laid financial plans. Dispelling these myths is the first step toward optimizing your retirement income and ensuring you’re fully benefiting from your federal benefits under the Federal Employees Retirement System (FERS). We will delve into the top 11 common misconceptions we see and equip you with the knowledge to make informed decisions about your retirement savings. Also, check out our TSP Common Misconceptions & Mistakes to avoid.

1. My income is too high to contribute into Roth TSP

There are no income limits for Roth TSP! We often hear that federal employees have not been contributing to Roth TSP because their income is too high. These income limits relate only to outside Roth IRAs. You can earn well above the income limits that are required for Roth IRAs and there will be no issue.

2. Contributing the max into the Roth TSP will result in losing the 5% government match. At least 5% must go to traditional TSP to receive the match.

You may contribute the max into Roth TSP and still receive the 5% TSP match. The government will not place your match into Roth. 100% of the government match goes into traditional TSP.

3. I’ll max out my TSP early in the year to allocate more funds to other areas for the remainder of the year.

Ensure you maximize your Thrift Savings Plan (TSP) contributions across all your pay periods in the year, typically 26. It’s crucial not to hit the maximum contribution limit too early, risking missing out on TSP matching funds. Divide the maximum contribution limits of $23,000 or $30,500 by the number of pay periods you have. For instance, reaching the max by June 1st means forfeiting half of the year’s potential match (2%). Repeating this error throughout your federal career could result in significant financial loss, potentially totaling tens of thousands of dollars. For more insight on matching funds, see TSP Matching Explained: How to Supercharge Your Retirement Savings.

If you are on 26 pay periods:

- $884 per pay period for $23,000

- $1,173 per pay period for $30,500

4. The S fund is a small cap fund

The TSP designates the S fund as a “Small Cap Stock Index Investment Fund,” which can be misleading. Its goal is to mirror the Dow Jones U.S. Completion Total Stock Market Index. This fund encompasses a mix of large, mid-sized, and small companies. Understanding the composition of the companies within the S fund is important for an effective investment strategy. For deeper insight into TSP fund performance, see Exploring TSP Funds: Share Price History and Rates of Return.

5. I will receive a 10% penalty for withdrawing before age 59 ½

This one depends. There are special exceptions that are only applicable to TSP retirees. If you meet one of the following you are exempt from the 10% penalty if withdrawing before age 59 1/2.

- Retirement in or after the year the account holder turns 55

- Public safety employees who retire in or after the year they turn 50

- Phased retirement

- Payments under certain qualified court orders (e.g., divorce, child support, etc.)

6. The TSP annuity option is owned by TSP

When opting for an annuity within your TSP, it’s vital to understand that TSP does not manage the annuity directly; it’s handled by an external provider. Presently, MetLife serves as the vendor for the annuity option. Your annuity will transition from TSP administration to MetLife. It’s important to note that selecting the single life annuity option will not leave the remaining balance in your TSP to your family or beneficiaries. For more details on annuities, see TSP Withdrawal Options: Installments, Payments, and Annuities.

7. Limited to one withdrawal every 30 days

Technically not true. You can receive an installment payment and a partial withdrawal. You may choose to receive installments from your account monthly, quarterly, or annually. In addition, you can receive a distribution of all or part of your TSP account. There is no limit on the number of partial distributions you can take, but TSP will not process more than one in any 30-day period.

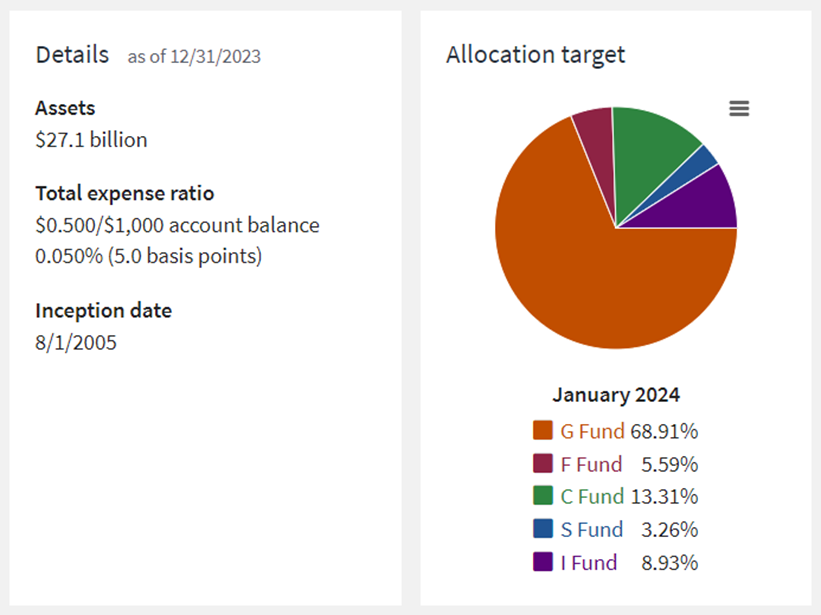

8. Matching the L fund with my retirement date takes care of my investment strategy

Just choose the L fund that corresponds with your retirement date and be done, right? The common set-it-and-forget-it strategy. While this statement may hold true during the initial stages of one’s career, the complexity of investment strategy changes upon retirement. Maintaining funds in the L Income Fund would lead to holdings predominantly in the G Fund (69%) and the F Fund (5.60%), totaling nearly 75% of the portfolio invested in cash and bond equivalents. Relying solely on the L Income Fund to generate retirement income may run the risk of not keeping up with inflation and potentially running out of money too soon.

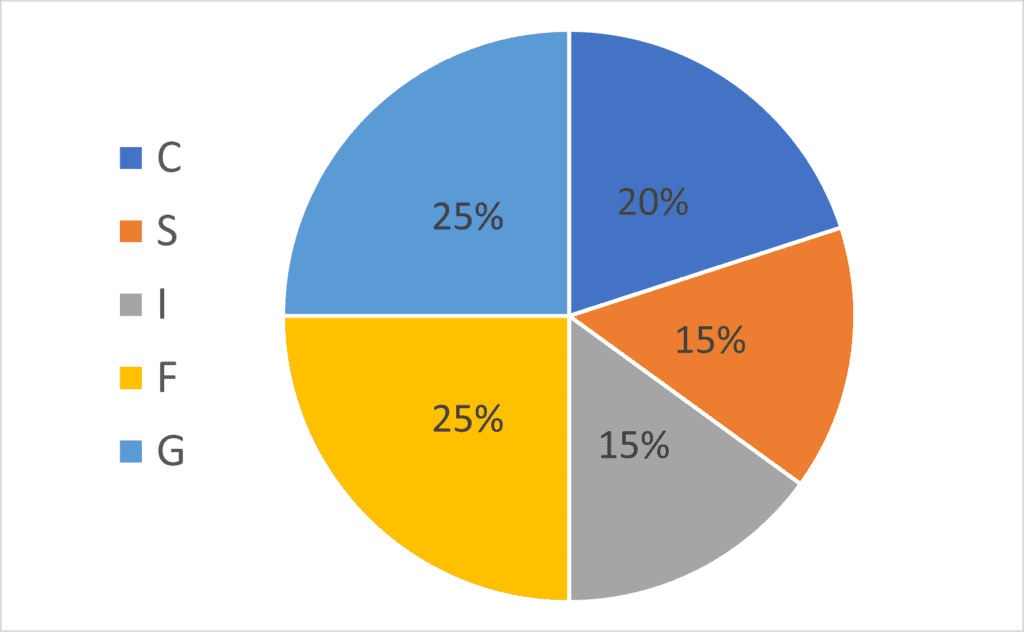

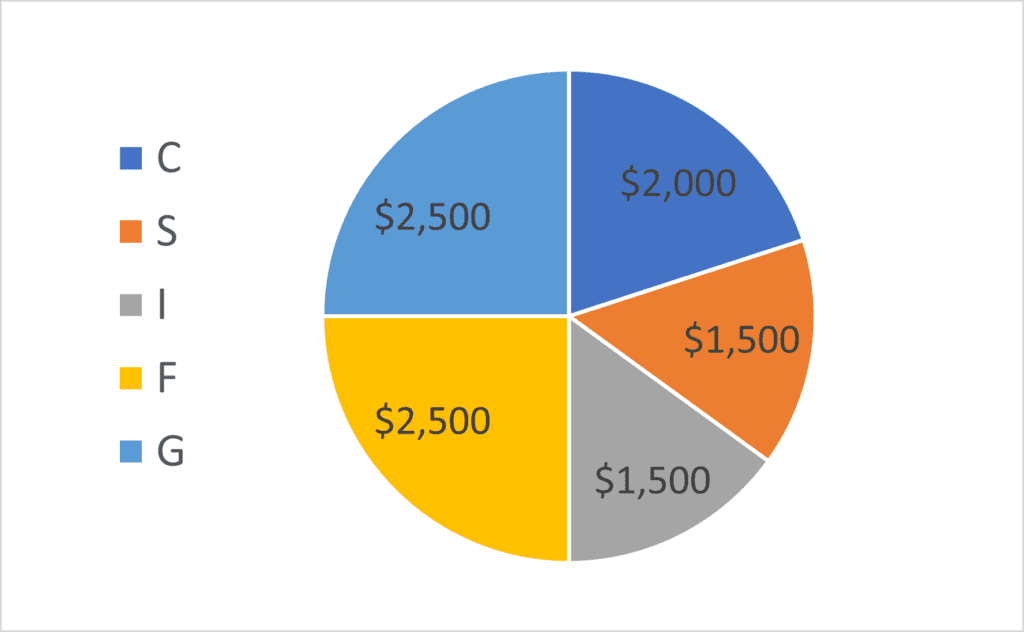

9. At retirement, I can select the fund from which I withdraw my investments

If you take a withdrawal, the money must come out pro rata based on your investment allocation. You are unable to select one fund to withdraw the money from. Below shows an example of a $10,000 withdrawal.

10. Misunderstanding of TSP loans

While the interest paid on a TSP loan is returned to yourself, two main downsides are often disregarded. Firstly, the loan amount doesn’t accrue growth based on your investment choices. Secondly, you face double taxation on the interest paid. When repaying interest into the TSP loan, you’re using after-tax funds, which are taxed again upon withdrawal at a later date.

More info: Thrift Savings Plan Loan – How Does It Work?

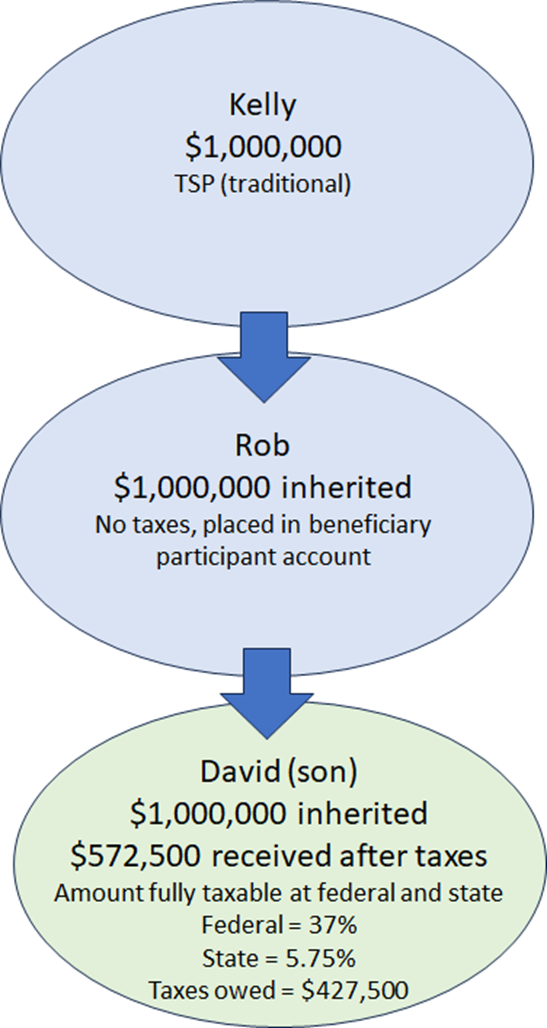

11. My beneficiary will inherit TSP tax-deferred

True and false.

True = your primary beneficiary will receive TSP funds into a beneficiary participant account (tax-deferred)

False = beneficiary of a beneficiary participant will receive TSP funds into a beneficiary participant account (tax-deferred)

There are no issues if a spouse (or primary beneficiary) receives the TSP in the event you predecease him/her. What happens when a beneficiary participant dies? The money cannot remain in the Thrift Savings Plan. The payments must be made directly to whom the beneficiary participant has chosen. The beneficiary of a beneficiary participant will be taxed at 100% of the account value at federal and state taxes. Consequently, the TSP funds cannot be rolled over into another beneficiary participant account to continue the deferral of taxes.

For example, say you predecease your spouse. Your spouse receives the TSP funds into a beneficiary participant account. When your spouse passes away, the funds go to your son or daughter. In this scenario, the full amount received will be taxable. The children will be unable to place these funds into a beneficiary participant account and could be taxed at the highest tax bracket.

More info: TSP Inheritance Issues – 100% Taxed to a Beneficiary

Why TSP is Bad?

We hear this question often and federal employees are wondering why TSP is bad. There are pros and cons to every work retirement plan and TSP is no exception. Each individual needs to weigh their specific financial situation to see if it aligns with their personal and financial goals. At PlanWell, you can sit with a Fed-Expert financial advisor for federal employees who specializes in helping career federal employees understand what is best for their unique situation.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciary® (AIF®). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Still wondering why TSP is bad? Want to have PlanWell host a federal retirement seminar for your agency? Reach out and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting.

Why TSP is Bad?

Federal employees need to understand why TSP is bad and why is TSP good. Working with a Fed-Expert Financial Advisor can help you understand what TSP does well and where it lacks. It is not a simple answer that leads to why TSP is bad. Thoughtful planning goes into understanding your unique situation to determine what is best for you and your family.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.