FERS Retirement Calculator and Federal Retirement Calculation Mistakes to Avoid

When estimating the retirement benefit for federal employees under the Federal Employees Retirement System (FERS), there are some common mistakes that can derail federal retiree's financial goals after leaving their federal job. Looking at each component of the FERS annuity computation, this article will highlight the biggest errors most employees make when estimating their income in retirement. After that, we'll examine how the federal retirement calculator provides the best possible estimate for federal employees developing their financial plan.

Top Errors Federal Employees Make When Calculating FERS Pension

When planning for retirement, there are several misconceptions federal employees make that can result in a lower-than-expected standard of living after retiring. To avoid any costly errors, understanding your federal retirement benefits is key to a achieving prosperity after committing your career to public service in the government. Here are the top three errors that financial advisors for federal retirement see most often.

Miscalculation of the FERS High-Three Salary

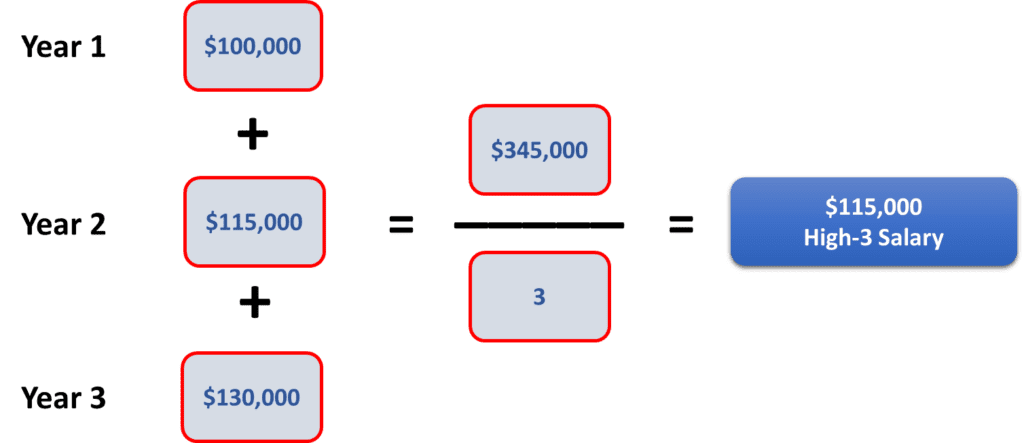

When figuring out the amount of a FERS annuity benefit, several key components are used to determine your estimated pension. One of these is the high-3 average salary, which is the highest average basic pay you earned during any three consecutive years of federal service. This is not tabulated by calendar years, but by 36 months, and is typically - but not always - the last three years of federal pay. Many use an excel spreadsheet to compute the final figure used in the retirement equation, but this method is prone to inaccuracies. Read this article to learn how the high-three average salary for FERS could become a "High-5."

Other key aspects to remember when figuring out the high-3 average for federal retirement:

- Locality pay is included

- Bonuses, the lump-sum payout of unused annual leave, and VSIPs are not included

- Only complete months can be used

- Unused sick leave can impact years of creditable service, but not the high-3 figure.

Confusing Creditable Service, Eligibility Requirements, and Unused Sick Leave

Besides the salary, the calculation for federal retirement benefits under FERSalso takes into account years of creditable service. Knowing what types of service are included is vital when estimating a future FERS annuity. Seasonal and temporary appointments are typically not creditable but part-time jobs and military service are. If FERS contributions were made while employed, or a military service deposit was completed, then this service can be included. If contributions to the federal retirement system were refunded, then a redeposit must be made before the retirement application is finalizedfor those years to count. And while unused sick leave will boost the number of years used in the computation, that increase does not carry over to eligibility requirements. For example, if you retire at MRA (minimum retirement age) with 29 years of service and unused sick leave raises that number to 30, you will still face an age reduction penalty with an immediate pension. You need to actually have 30 years of service for the unreduced annuity.

Learn all about creditable and non-creditable service at a free online seminar for federal retirement.

Misunderstanding Rules Surrounding the 1.1 Multiplier

To be clear, a FERS pension is determined by multiplying the High-Three average by years of creditable service by either 1.0% or 1.1%. The 1.1 multiplier (effectively boosting one's pension income by 10 percent) can only be used if retiring on an immediate annuity (not postponed or deferred) at age 62 or older with at least 20 years of creditable service, although unlike eligibility requirements, unused sick leave can be used to receive the 10% pension boost.

Making errors when figuring out your retirement plan can have devastating consequences. This is why federal employees need an advisor they can trust.

What is the FERS Retirement Calculator and How Does it Work?

The FERS Retirement Calculator is an essential tool designed to help federal employees estimate their retirement benefits under the FERS retirement system. This calculator takes into account various factors such as years of service, high-3 average salary, and age to provide an estimate of the pension you can expect to receive upon retirement. By inputting specific data, federal employees can gain a clearer picture of their financial future and make necessary adjustments to their retirement planning strategy. Don't forget FERS retirement will be taxed and the calculator provides the gross pension amount.

How to Calculate Your Federal Retirement Benefits Accurately

Calculating your retirement benefits accurately is essential for effective retirement planning after your federal career. By understanding the steps involved in the FERS pension calculation, you can ensure that you are on track to meet your financial goals. This involves gathering all necessary information, understanding the impact of your retirement service computation date, and avoiding common mistakes that could lead to inaccurate estimates.

Steps to Calculate Your FERS Pension

To calculate your FERS pension, start by determining your high-3 average salary and your total years of service. Multiply your high-3 average salary by the applicable pension multiplier (1% or 1.1% depending on your age and years of service) and then by your total years of service. This will give you an estimate of your annual pension. It is important to consider any reductions that may apply, such as those for early retirement or survivor benefits, to get a more accurate picture of your net pension.

Importance of the Retirement Service Computation Date (RSCD)

The Retirement Service Computation Date (RSCD) is a crucial factor in calculating your federal retirement benefits. It determines your total years of creditable service, which directly impacts your pension amount. It accounts for any breaks in service and periods of non-creditable service, ensuring that your years of service are accurately reflected in your retirement calculation. Federal employees should verify their RSCD with their human resources department to avoid any discrepancies in their retirement benefits. The SCD (no "R") is used for leave purposes.

Eligible to Retire? Subscribe to Our Biweekly Newsletter and Receive a Free FERS Handbook!

Common Mistakes in Federal Retirement Calculations

Federal employees often make mistakes in their retirement calculations that can lead to inaccurate estimates of their benefits. Common errors include miscalculating the high-3 average salary, overlooking the impact of sick leave on creditable service, and failing to account for reductions due to early retirement or survivor benefits. To avoid these pitfalls, it is essential to double-check all calculations andconsult with a retirement specialist if needed.

How to Plan for FERS Federal Retirement: Strategies and Tips

Effective retirement planning is essential for federal employees to ensure a comfortable and secure retirement. By developing a comprehensive retirement strategy, maximizing your FERS retirement benefits, and understanding the role of FEHB and FEGLI in retirement planning, you can set yourself up for financial success in your golden years.

Schedule a meeting with a fed-expert financial planner.

Plan Your Federal Retirement Journey: Maximizing Your Federal Benefits in Retirement

To maximize your FERS retirement benefits, it is important to understand the factors that influence your pension and take steps to optimize them. This includes maximizing your high-3 average salary, the highest 36 consecutive months of basic pay, increasing your years of service, and strategically planning your retirement date. Additionally, federal employees should consider contributing to the Thrift Savings Plan (TSP) to supplement their FERS pension and Social Security benefits.

Use our TSP Calculator to further estimate income in retirement.

Understanding the Role of FEHB and FEGLI in Retirement Planning

The Federal Employees Health Benefits (FEHB) program and the Federal Employees' Group Life Insurance (FEGLI) program play important roles in retirement planning. FEHB provides health insurance coverage for federal retirees, while FEGLI offers life insurance options. Understanding how these programs work and how they fit into your overall retirement strategy is essential for ensuring you have the coverage you need in retirement.