How to Calculate Your FERS Retirement Annuity: A Comprehensive Guide for Federal Employees

For federal employees, planning for retirement means building a strategy for their three potential sources of income: social security retirement benefits, investments in their Thrift Savings Plan account, and then their FERS pension. The Federal Employees Retirement System (FERS) provides a guaranteed pension, which is a significant component of a federal employee's retirement benefits. Understanding how to calculate your FERS retirement annuity is essential for effective retirement planning. This guide will walk you through the steps involved in calculating future income from a FERS annuity, definitions of the components involved, and how to build an effective strategy in order to get the most money from a FERS annuity after retiring from the federal government.

If you are looking for a FERS Retirement Calculator, Try our FREE Online Tool for Calculating Your future FERS Income

How to Calculate Your FERS Retirement Pension

Steps for Figuring Out Your FERS Pension Calculation

Calculating your FERS retirement income involves several steps.

- First, determine your high-3 salary, which is the average of your highest three consecutive years of basic pay.

- Next, calculate your years of creditable service, which includes all periods of federal service that count towards your retirement.

- The basic formula for calculating your FERS annuity is 1% of your high-3 salary multiplied by your years of service. If you retire at age 62 or later with at least 20 years of service, the multiplier increases to 1.1%. This calculation provides an estimate of your annual FERS pension.

Calculating Your Federal Retirement Benefits

Basic Calculation for Federal Employee Retirement System

You will use the basic calculation if you fall under one of the following:

Retiring under age 62 with any number of years of service

OR

Retiring after age 62 with less than 20 years of service

| High Three Avg. Salary | x Years of Creditable Service |

Pension Multiplier: x 1.0% |

= Gross Pension Amount |

Bonus Calculation with 1.1 percent Multiplier

You will use the basic calculation if:

Age 62 or After With at Least 20 Years of Service

| High Three Avg. Salary | x Years of Creditable Service |

Pension Multiplier: x 1.1% |

= Gross Pension Amount |

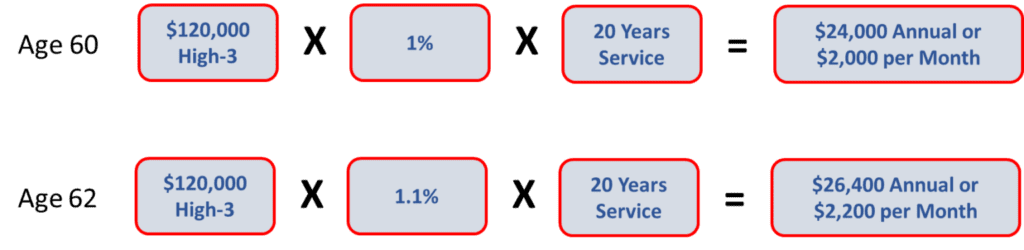

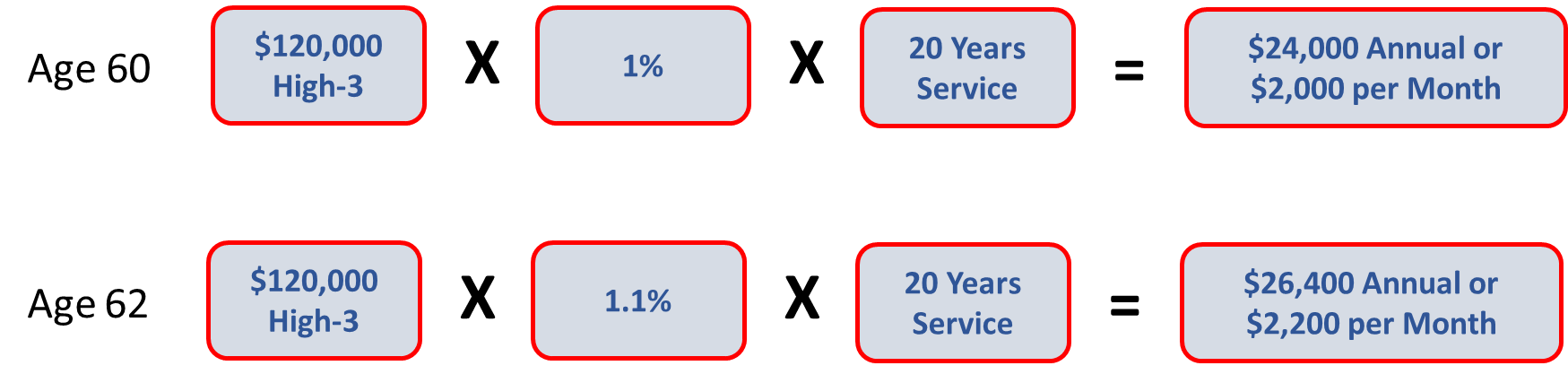

Basic Annuity (1%) vs. Bonus Calculation (1.1%) – The 10% Bonus

The decision to retire before age 60 or after 62 can be a game changer for your retirement. In the below example, you can see the increase just by retiring after 62 with the same high-3 and years of service. An early retirement can have a noticeable impact when considering an immediate retirement before the age of 62.

Components of the Annual Pension Calculation for FERS Employees

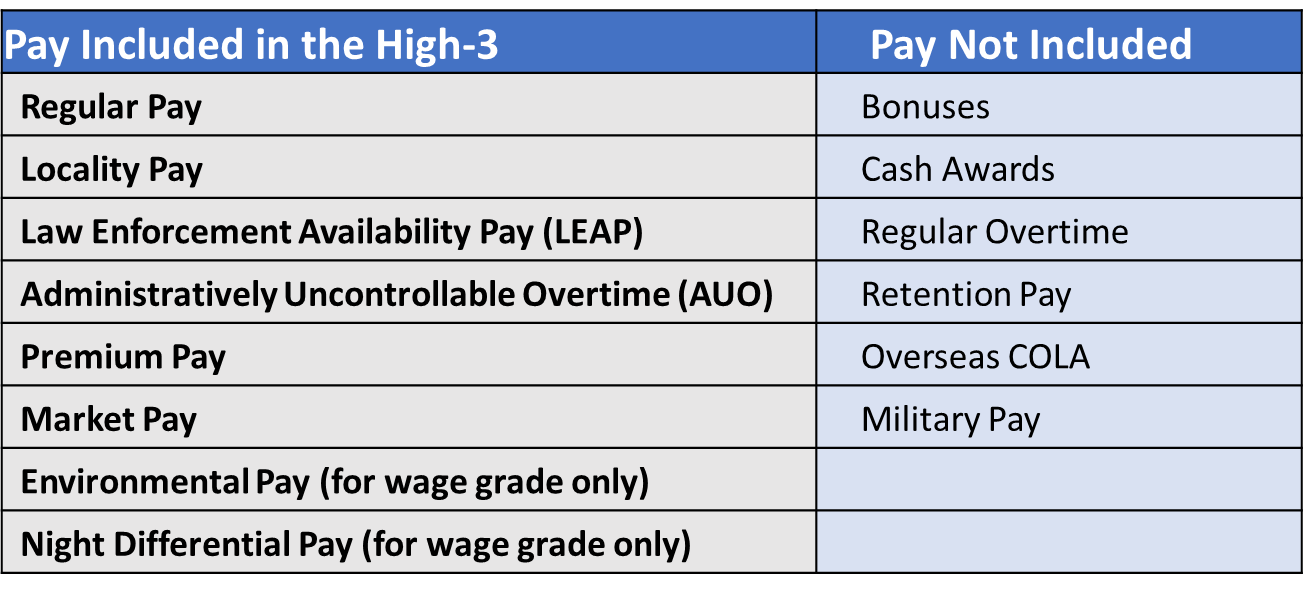

Figuring Out the High-3 Average Salary

The high-3 average salary represents the average of the highest three consecutive years of basic pay for federal careers and is used to calculate your retirement benefit. The higher your high three average salary, the larger your FERS annuity will be. More often than not, the average pay is comprised of the last 36 months' salary amounts before retirement. Both basic and locality pay is used when figuring out the average high-3 salary.

Years of Creditable Service and Sick Leave

The number of years of creditable service plays a significant role in determining your FERS pension. Each additional year of service increases your annuity by 1% of your high-3 salary. Therefore, federal employees with longer service periods receive higher retirement benefits. It's important to note that certain types of service, such as military service or periods of leave without pay, may also count towards your creditable service, potentially increasing your FERS annuity.

Types of Creditable Service:

- Service time from work

- Unused sick leave*

- Military time

- Made deposit to count towards civilian service

- Redeposit service

- Refunded pension contribution when leave

- Non-deductible Service (Temp/Intern)

- Federal service before 1/1/1989 but did not contribute to FERS (must buy back)

*Unused sick leave is converted into creditable service hours upon retirement. This extra time may count toward the retirement calculation, but it does not boost one's years in service in terms of eligibility for a retirement annuity.

Check out our free online tool for converting sick leave hours.

Resources to Help You Plan Your Federal Retirement

Tools to Help Federal Employees Map Out their Retirement

Our retirement calculators are invaluable resources for federal employees planning their retirement. These free online tools include:

- FERS Pension Calculator

- Thrift Savings Plan Calculator

- Sick Leave Converter

- FERS Supplement Calculator

Also - check out our Complete Guide to the Federal Employee Retirement System, which contains information on Special Retirement Provisions, the FERS Supplement, the minimum retirement age, disability retirement, and alternatives for FERS workers including postponed, deferred, and MRA+10 pension options.

If you're approaching retirement, check out our Online Workshops about FERS Retirement Benefits

OPM Retirement Services and Applying for FERS Benefits

The Office of Personnel Management (OPM) processes all FERS retirement applications, which are sent to the Iron Mountain facility in Pennsylvania for processing. Planning your retirement date around OPM's processing times can be a useful strategy for a more timely response from their retirement services division, but might dampen one's lump-sum from accumulated annual leave. But more importantly, feds will want to ensure they send a mistake-free retirement packet and that OPM, in turn, also doesn't make any errors when calculating your net pension.

Need personal help with preparing your retirement application? Meet with us.

What About Calculating a CSRS Pension?

While both FERS and CSRS (Civil Service Retirement System) are retirement systems for federal employees, they have distinct differences. CSRS, which was established in 1920, is a more traditional pension plan that does not include Social Security benefits and more restricted when it comes to investing in the TSP. In contrast, FERS integrates Social Security and offers more flexible retirement savings options through the TSP. Understanding these differences is crucial for federal employees who may have service under both systems, known as CSRS Offset, which affects how their retirement benefits are calculated.

At 41 years and 11 months of service, CSRS annuities equal 80% of their high-3 salary. At that point, no more service will increase a CSRS employee pension estimate.

If you have a CSRS component as a part of your federal retirement benefits, reach out to an advisor here at PlanWell Financial to help you navigate your retirement from the federal government. Thank you for your service!