Comparing Federal Employee Group Life Insurance (FEGLI Option B) with Term Life Insurance: Which is Right for You?

As a federal employee, you can access some pretty sweet benefits, including the Federal Employee Group Life Insurance (FEGLI) program. But within FEGLI, there are choices to make, and one of the biggest is Option B. So, is Option B your financial hero, or should you be looking elsewhere, like term life insurance? Let’s dive in and compare!

What is Federal Employee Group Life Insurance?

Simply put, FEGLI is a life insurance program offered to federal employees and retirees. Because the employer provides it and everyone qualifies for it when you start work, it is a “group life insurance program.” Many employers in the private sector and state government offer a similar type of benefit. Lastly, FEGLI itself is not a purely federal program. It is a federal private partnership with MetLife.

Parts of FEGLI Coverage: Basic, Option A, Option B, and Option C

There are 4 major parts of FEGLI. Basic coverage provides a life insurance amount that’s close to one time of your annual income. Option A is $10,000 of coverage. Option B is multiples of additional coverage based on your income. Lastly, Option C provides coverage for your spouse and children. To learn more about each option, please review our article on Maximizing Federal Employee Group Life Insurance (FEGLI) Benefits (planwellfp.com).

FEGLI Option B

We want to focus on Option B for this article since most federal employees don’t understand some important aspects. The most significant benefit of Option B is that you do not need a health exam and are eligible to increase the insurance amount to five times your income. Moreover, the coverage goes up as your income goes up. So Option B coverage grows over time. Lastly, it is relatively inexpensive when you are young.

What are the Downsides?

With the pros, there are some cons. While the coverage increases, the cost increases since the premiums are determined per thousand of coverage. What’s worse is that the expense is based on an age band. It is inexpensive when you are young. However, as we age, the cost for Option B skyrockets. You can see the detailed rates per thousand below.

| Age Group | Bi Weekly | Monthly |

|---|---|---|

| Under 35 | $0.02 | $0.043 |

| 35 ~ 39 | $0.02 | $0.043 |

| 40 ~ 44 | $0.03 | $0.065 |

| 45 ~ 49 | $0.06 | $0.130 |

| 50 ~ 54 | $0.10 | $0.217 |

| 55 ~ 59 | $0.18 | $0.390 |

| 60 ~ 64 | $0.40 | $0.867 |

| 65 ~ 69 | $0.48 | $1.040 |

| 70 ~ 74 | $0.86 | $1.863 |

| 75 ~ 79 | $1.80 | $3.900 |

| Over 80 | $2.88 | $6.240 |

The rate increase is minor when you are under 44, with the first big jump after you turn 45. While the $0.06 per thousand rate is low, that is a 100% increase! The cause doubles again at 55 and 60.

The Cost Difference Between Age 45 vs 55

Using the table above, we can show how the age band will increase the insurance cost, assuming the insurance amount stays the same.

| Age 45 | Age 55 | |||

|---|---|---|---|---|

| Life Insurance Amount | Bi-Weekly | Monthly | Bi-Weekly | Monthly |

| $250,000 | $15.00 | $32.50 | $45.00 | $97.50 |

| $500,000 | $30.00 | $65.00 | $90.00 | $195.00 |

As you can see, the cost will triple over 10 years. This may not be a good option if you are healthy.

FEGLI Option B is Group Term Life Insurance

Federal Employees don’t realize how group life insurance determines its cost. Because it has to accept everyone, it has to price in the cost for healthy and not-so-healthy people. In essence, healthy folks are subsidizing the cost of not-so-healthy people. Women are subsidizing for men since women tend to live longer. Non-smokers are subsidizing smokers since smoking is connected to various health issues.

This means that if you are a non-smoking healthy woman, you are paying a lot for life insurance using FEGLI.

Possible Alternative: Term Life Insurance

This kind of life insurance option is available in the private sector. It does require you to go through an application process and take a physical. However, because the insurance company can rate your health, they could offer you a cost lower than what you pay in a group setting.

Term policies do not build any cash or residual value. It only pays out the benefit at death. Some policies do have a feature that allows you to convert to a different kind of life insurance policy or pay out early if you have a terminal illness. Lastly, it is a contract between you and the insurance company. As long as you pay, the insurance company will pay the benefit in the event of your death. However, you are free to stop the policy at any time.

How Does Term Policies Work?

The “Term” refers to a time period. During this time period, the insurance cost is fixed and cannot change. So instead of seeing your cost increase every 5 years, you can lock in a rate that’s 10, 20, or even 30 years. You can also select different insurance providers since each may review health situations differently and find the best deal. Most importantly, you can choose to cancel the policy at any time. Just because you got a 30 year policy, you do not need to keep it for the entire time.

Cost Comparison

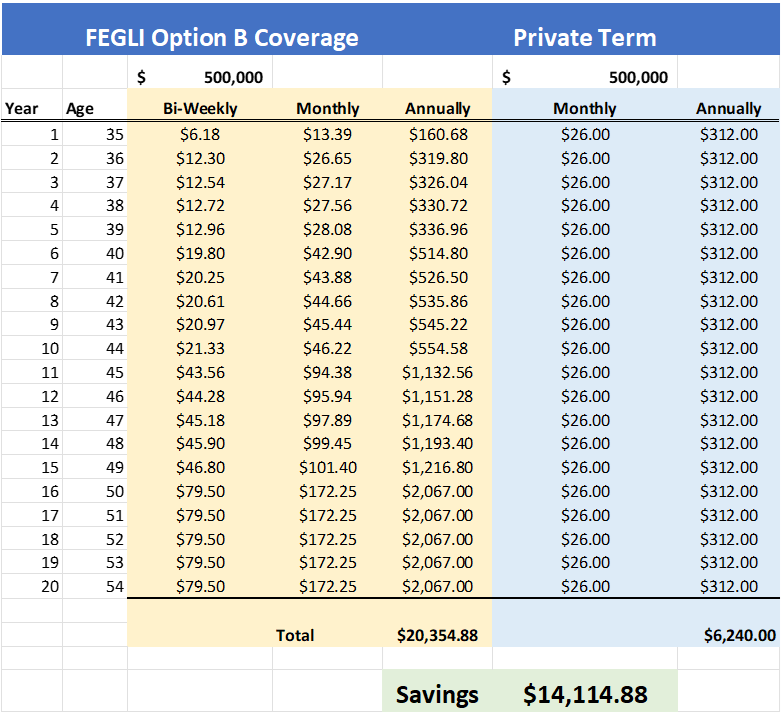

When considering and reviewing life insurance coverage, it is vital to have some context. Here is an example of a healthy man aged 35 with $500,000 in FEGLI coverage vs Term Life Policy over 30 years.

As you can see, the cost of private life insurance is higher initially. Over time, because the cost of private insurance is fixed, you may end up saving $14,114.88 in 20 years. The savings will be even higher if we compare it over 30 years.

Which is better for Federal Employees?

Instead of considering this question in general terms, we need to look at your situation. If you are young, healthy, and do not smoke, getting a term life insurance policy makes sense. If you have health issues, it may be better to keep FEGLI instead since you may not qualify for insurance otherwise. The key is NOT to make changes without doing your homework. If you decide to replace FEGLI with Term, apply for Term insurance first. Get approved and pay for the policy, before replacing your FEGLI. Do not cancel any existing life insurance ahead of being approved.

Converting Term Life to Permanent Life Insurance

Some insurance providers will allow you to convert all or a portion of your existing term life insurance policy to one that will not expire. The benefit is that you do not need to go through a medical and no health questions. This may be a good strategy if your health changes and you want to maintain the policy beyond the term period. The critical thing to understand is that every insurance company’s offer to convert is different, and you may only have a set time frame to exercise this option. For example, you may not be able to convert in the last year of your term policy. It is up to you to make sure what your options are.

Other Private Sector Life Insurance

Other kinds of life insurance products may fulfill different goals. Each is unique, and you need to speak to an advisor with your interest at heart. Many insurance agents want to sell the most extensive policy with bells and whistles. You need to decide if paying for all of that makes sense. Remember who is the life insurance benefit for. Remember that goal and ask yourself, how does this policy fit your insurance needs? Do the extra options enhance or distract me from my purpose?

Whole Life

The original permanent insurance is a whole life policy. The goal is to have a fixed monthly life insurance cost until you pass away. In order to do that, you would pay a much higher cost and build up cash value within the policy. The insurance company will offer you a fixed interest rate on the cash, and you will receive interest and dividends over time. As the policy cash grows, you can withdraw the money or borrow the cash for other needs. However, remember that if you take out too much, there may not be enough funds in the policy to pay for the cost of insurance when you are older.

Variable Life (VL) or Variable Universal Life (VUL)

Variable life works very similarly to whole life insurance. The difference is that you can invest the cash in the stock market instead of getting a fixed interest rate from the insurance company. Since you are investing, you could lose money in the market. Moreover, you will pay additional costs from the mutual funds within the policy.

Index Universal Life (IUL)

The IUL is the newest kind of policy. There are many choices in the marketplace, and they are complicated products. You do not get a fixed interest rate from the insurance company. Instead, the interest you receive is based on an annualized market return (the index). However, you are not invested directly in the market, so you do not get all the gains.

On the other hand, you would not take any losses if the market were to go down. The key is to make sure you understand how the index works. Moreover, IUL may include additional features called riders that add to the insurance cost.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®) and Chartered Federal Employee Benefits Consultants (ChFEBC℠). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars here! Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Interested in having PlanWell host a federal retirement seminar for your agency? Reach out, and we can collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting here.