Renting vs. Owning in Retirement: Pros and Cons for Retirees

As retirees transition into their next phase of life, the decision of whether to rent or own a home in retirement becomes increasingly significant. Both options have their own set of pros and cons, and understanding the factors at play can help retirees make an informed choice that aligns with their financial and lifestyle goals.

Is Renting a Better Option for Retirees?

When considering renting in retirement, there are several critical factors that retirees should take into account. These may include the flexibility of not being tied down to a property, the potential relief from maintenance responsibilities, and the ability to free up equity for other purposes. In retirement, if you own a home you have the option to sell and invest the equity to generate income for retirement. Owning a home keeps the equity illiquid and unable to generate income.

Retirees must carefully weigh the pros and cons of renting. While renting provides financial flexibility, it also means having to deal with potential rent increases and the lack of long-term equity accumulation. Deciding between renting and buying requires a thorough evaluation of individual circumstances and retirement plans.

Whether to rent or buy in retirement depends on various personal factors, such as desired financial stability, freedom from homeownership obligations, and the availability of funds for a down payment or ongoing rent payments.

Pros and Cons of Homeownership for Retirees

For retirees, homeownership offers the possibility of building equity in a property. This can be a valuable asset that contributes to your overall financial security and retirement planning. However, owning a home also comes with downsides such as the annual maintenance costs that will inevitably occur. A big differentiator between owning vs. renting is the desire to spend on upgrades and renovations to the home. This is often overlooked when comparing the differences between owning vs. renting.

While building equity through homeownership can be advantageous, retirees should be aware of the ongoing expenses related to maintaining a property. It’s essential to factor in these costs when determining whether owning a home is the best choice for their retirement years. As you age, you may no longer be able to do yard work and house maintenance yourself creating an increased expense.

The decision to rent or buy in retirement requires careful consideration of how homeownership may align with retirement income and whether it offers the desired level of financial stability.

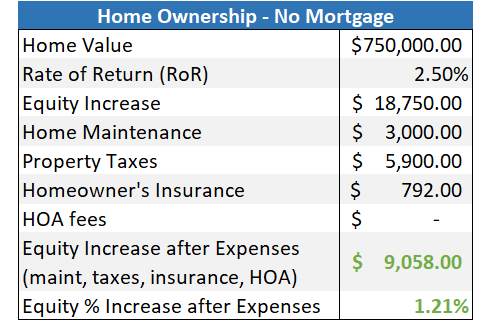

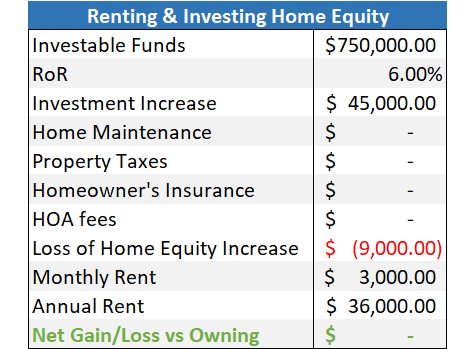

Owning vs. Renting in Retirement

*The example above is a very basic difference of owning vs. renting. Consideration will need to be taken for your indiviudal tax situation.

Thoughtful planning must be taken when considering a rent vs. buy situation. If you own a home, the sale of the house and proceeds can now be used to generate income. In the example above you would breakeven with a rent payment of $3,000/month. If you were to increase the cost of home maintenance, renovations, or upgrades, then renting is now a better financial option.

Renting can be very advantageous in retirement. As you age you may not be handle or want to deal with what comes with owning a home such as: maintenance on the residence, yardwork, renovations or remodels, or the possiblity of the house depreciating.

Considering Renting as a Retiree

When exploring the idea of renting in retirement, retirees should evaluate how it could potentially provide a better housing solution. Renting may offer the benefits of easier relocation, reduced maintenance responsibilities, and access to various housing options without having to commit to a long-term property.

Retiring individuals may find that renting is a better choice due to the flexibility it provides and the freedom from property ownership concerns. Deciding to rent or own a retirement home requires carefully assessing the pros and cons of each option in the context of individual retirement plans.

A seldom-discussed aspect is the potential financial advantage retirees may experience by renting rather than owning. It’s not only about homeowners dealing with property taxes, insurance, and annual maintenance; the decisive factor lies in the substantial expenses homeowners often incur for upgrades and renovations. Unlike homeowners, renters rarely contemplate tearing out and rebuilding their kitchens. Every homeowner can relate to the difference here and the huge costs we incur to make our homes our own.

Owning a Home in Retirement: Factors to Consider

Home equity can significantly influence the financial well-being of retirees. Owning a home may also offer the possibility of downsizing and selling the current property to free up funds for retirement or leveraging a reverse mortgage to access the equity in their home.

As retirees navigate the decision to own a home in retirement, the potential to downsize and sell their property becomes relevant. Selling a home can provide additional retirement funds, whereas leveraging a reverse mortgage offers a way to access home equity while continuing to reside in the property.

Consideration of whether to buy or rent in retirement necessitates evaluating how home ownership and its related financial implications align with retirement plans and long-term objectives.

Renting vs. Owning: Financial Considerations for Retirees

Property tax and homeownership costs should factor into the financial planning of retirees. Conversely, leasing a rental property allows for the flexibility of not being responsible for property taxes and ongoing maintenance. Incorporating housing costs into retirement planning is essential for retirees exploring whether to rent or buy in retirement.

Retiring individuals must weigh the potential tax deduction benefits of owning a home vs. the typically lower housing costs associated with renting. Making an informed housing decision in retirement involves a comprehensive evaluation of the financial implications of renting versus owning, as well as how each option aligns with their retirement income and goals.

Deciding whether to rent or buy in retirement involves carefully examining how housing expenses and ownership responsibilities fit within the overall retirement plan and desired financial stability.

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciaries (AIF®). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars. Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Want to have PlanWell host a federal retirement seminar for your agency? Reach out and we’ll collaborate with HR to arrange an on-site FERS seminar.

Want to fast track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a financial advisor for federal employees today. You can schedule a one-on-one meeting at your convenience.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.