Medicare Advantage (Part C) vs Medicare Supplement (Medigap)

Medicare Advantage (Part C) and Medicare Supplement Insurance Plans also known as Medigap are crucial elements to your financial wellbeing in retirement. Big decisions must be made the year you turn age 65 (or at retirement if after age 65). Both Medicare Advantage and Medigap will pay some or all of the costs not covered by Original Medicare (Parts A and B). There are distinguishing features that each offers so it is important to take the time to do your research before making the decision the is best for you.

Below we will cover Original Medicare, Medicare Advantage, and Medigap.

Original Medicare

When you first sign up for a Medicare plan and during certain times of the year, you can choose how you get your Medicare coverage. There are 2 main ways to get Medicare: Original Medicare (Part A and Part B) or a Medicare Advantage Plan (Part C). Some people need to get additional coverage, like Medicare drug coverage (Part D) or a Medicare Supplement Insurance (Medigap).

- Original Medicare includes Medicare Part A (Hospital Insurance) and Part B (Medical Insurance)

- You can join a separate Medicare drug plan to get Medicare drug coverage (Part D).

- You can use any doctor or hospital that takes Medicare, anywhere in the U.S.

Important! – Generally, you need to pay a portion of the cost for each service Original Medicare covers out-of-pocket. There is no limit to what you may pay in a year unless you have other coverage, such as a Medicare Supplement, Medicaid or employee or union coverage, or you enroll in a Medicare Advantage plan.

What are the costs and coverage for Original Medicare?

|

Costs |

Part A |

Part B |

|

Premium |

$0

(for most people if you paid Medicare taxes long enough while working -

generally at least 10 years) |

$164.90/month

($174.70 in 2024) or higher depending on your income |

|

Deductible |

$1,600 ($1,632 for 2024) for each inpatient hospital benefit

period, before Original Medicare starts to pay. There’s no limit to the number of benefit periods you can

have in a year. This means you may pay the deductible more than once in a

year. |

$226 ($240 in 2024) before Original Medicare starts to

pay. Deductible is paid once a year. |

|

General Costs for Services |

Co-insurance

~20% of the Medicare-approved amount for most doctor services while you’re a

hospital inpatient |

Co-insurance

~20% of the Medicare-approved amount for most doctor services while you’re a

hospital inpatient |

|

Inpatient Stay |

·

Days 1-60: $0 after you pay your Part A

deductible. ·

Days 61-90: $400 ($408 in 2024) copayment each

day. ·

Days 91-150: $800 ($816 in 2024) copayment

each day while using your 60 lifetime reserve days. ·

After day 150: You pay all costs. |

20% of the Medicare-approved amount for most doctor

services while you’re a hospital inpatient |

|

Skilled Nursing Facility Stay |

·

Days

1-20: $0 copayment ·

Days

21-100: $200 ($204 in 2024) copayment each day. ·

Days

101 and beyond: You pay all costs. |

$0 for

Medicare approved |

|

Home Health Care |

·

$0 for covered home health care services ·

20% of the Medicare-approved amount for

durable medical equipment (like wheelchairs, walkers, hospital beds, and

other equipment) |

·

$0 for covered home health care services ·

20% of the Medicare-approved amount for

durable medical equipment (like wheelchairs, walkers, hospital beds, and

other equipment) |

|

Hospice Care |

·

$0

for covered hospice care services. You may also pay: A copayment of up to $5 for each

prescription drug and other similar products for pain relief and symptom

control while you're at home. What if my hospice care doesn't

pay for my drug? 5% of the Medicare-approved

amount for inpatient respite care. |

N/A |

|

Outpatient Hospital Care |

N/A |

·

~ 20% of the Medicare-approved amount for

doctor and other health care providers’ services. ·

You’ll also pay a copayment to the hospital

for each service you get in a hospital outpatient setting (except for certain

preventive services). In most cases, your copayment won’t be more than the

Part A hospital stay deductible amount. |

|

Clinical Lab Services |

$0 for covered clinical

laboratory services |

$0 for covered clinical

laboratory services |

|

Description |

|

|

Benefit Period |

Start: The day you're admitted as an inpatient End: When you haven't received any inpatient hospital care for 60 days in a row |

|

Inpatient Stay |

Inpatient care is care provided in a hospital or other type of inpatient facility, where you are admitted, and spend at least one night—sometimes more—depending on your condition. |

|

Skilled Nursing Facility |

Skilled nursing care is provided by trained registered nurses in a medical setting under a doctor’s supervision. Patients may go from the hospital to a skilled nursing facility to continue recovering after an illness, injury or surgery. A skilled nursing facility provides transitional care. The goal is to get well enough to go home. |

|

Home Health Care |

This is NOT long-term care. Home health care is a wide range of health care services that can be given in your home for an illness or injury. Home health care is usually less expensive, more convenient, and just as effective as care you get in a hospital or skilled nursing facility (SNF). |

|

Hospice Care |

Hospice care is a special kind of care that focuses on the quality of life for people who are experiencing an advanced, life-limiting illness and their caregivers. Hospice care provides compassionate care for people in the last phases of incurable disease so that they may live as fully and comfortably as possible. |

Medicare Advantage (Part C)

If you have Part A and Part B, you can join a Medicare Advantage Plan, sometimes called “Part C” or an “MA plan.” This type of Medicare health plan is offered by Medicare-approved private companies that must follow rules set by Medicare. Most Medicare Advantage Plans include drug coverage (Part D). In addition, Medicare Advantage usually includes bonus benefits such as dental, vision, and hearing services.

An important distinction is that you are technically not on Original Medicare when using a Medicare Advantage plan.

Types of Medicare Advantage Plans

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Medicare Medical Savings Account (MSA)

- Private-Fee-for-Service Plan (PFFS)

- Special Needs Plan (SNP)

Original Medicare vs Medicare Advantage

|

|

Original

Medicare (Part A & B) |

Medicare

Advantage |

|

Cost (coinsurance and out-of-pocket) |

Pay ~20% of the Medicare-approved

amount after you meet your deductible (coinsurance). |

Out-of-pocket costs vary – plans may

have lower or higher out-of-pocket costs for certain services. You may also

have an additional premium. |

|

There’s no yearly limit on what you pay out-of-pocket. |

Plans have a yearly limit on what you pay out of pocket for services Medicare Part A and Part

B cover. Once you reach your plan’s limit, you’ll pay nothing for services

Part A and Part B covers for the rest of the year. |

|

|

You can choose to buy Medigap to help

pay your remaining out-of-pocket costs (like your 20% coinsurance). Or, you can use coverage from a former employer or union,

or Medicaid. |

||

|

Premium |

Part A

usually $0 and pay separate if you elect Part D. |

May have to pay the plan’s premium. Some plans may have a $0 premium and may

help pay all or part of your Part B premium. |

|

Part B = $164.90/month

($174.70 in 2024) or higher depending on your income. |

Must pay the Part B premium = $164.90/month

($174.70 in 2024) or higher depending on your income. |

|

|

Doctor & Hospital Choice |

You can go to any doctor or

hospital that takes Medicare, anywhere in the U.S. In most cases you don’t

need a referral to see a specialist. |

In many cases, you can only use

doctors and other providers who are in the plan’s network and service area

(for non-emergency care). You may need to get a referral to see a specialist. |

|

Coverage |

Original Medicare

covers most medically necessary services and supplies in hospitals, doctors’

offices, and other health care facilities. Original Medicare doesn’t cover

some benefits like eye exams, most dental care, and routine exams. |

Plans must

cover all medically necessary services that Original Medicare covers. Plans

may also offer some extra benefits that Original Medicare doesn't cover -

like certain vision, hearing, and dental services. |

|

Medicare Drug Coverage (Part D) |

Not included, must pay an additional

premium |

Included in most plans. |

|

Prior Approval |

In most

cases, you don’t need approval for Original Medicare to cover your services

or supplies |

In many

cases, you may need to get approval from your plan before it covers certain

services or supplies. |

|

Foreign Travel |

Original Medicare generally

doesn’t cover medical care outside the U.S. You may be able to buy a Medicare

Supplement Insurance (Medigap) policy that covers emergency care outside the

U.S. |

Plans generally don’t cover

medical care outside the U.S. Some plans may offer a supplemental benefit

that covers emergency and urgently needed services when traveling outside the

U.S. |

|

Medigap Eligible |

Yes |

No |

Medicare Supplemental Insurance Plan (Medigap)

Important to note that you would be on Original Medicare and in addition the Medicare Supplement Insurance Plan (Medigap). Medigap is additional insurance you can buy from a private insurance company to help pay your share of costs in Original Medicare. You can only buy Medigap if you have Original Medicare. Generally, that means you must sign up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) before you can buy a Medigap policy.

All Medigap policies are standardized. This means they offer the same basic benefits no matter where you live or which insurance company you buy the policy from. There are 10 different types of Medigap plans offered in most states, which are named by letters: A-D, F, G, and K-N. Price is the only difference between plans with the same letter that are sold by different insurance companies.

If you have a Medigap policy and get care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then, your Medigap policy will pay its share. You’re responsible for any costs that are left.

Once you buy a policy, you’ll keep it as long as you pay your Medigap premiums. All standardized Medigap policies are automatically renewed every year, even if you have health problems. Your Medigap insurance company can only drop you if:

- You stop paying your premiums

- You weren’t truthful on the Medigap policy application

- The insurance company goes bankrupt or goes out of business

Medigap plans sold after 2005 don’t include prescription drug coverage. So, if you enroll in Medigap for the first time, it won’t include drug coverage. If you want prescription drug coverage, you can join a separate Medicare drug plan (Part D).

|

Plan A |

Plan B |

Plan C |

Plan D |

Plan F* |

Plan G* |

Plan K |

Plan L |

Plan M |

Plan N |

|

|

Part A coinsurance and hospital costs up to an

additional 365 days after Medicare benefits are used up |

ü |

ü |

ü |

ü |

ü |

ü |

ü |

ü |

ü |

ü |

|

Part B coinsurance or copayment |

ü |

ü |

ü |

ü |

ü |

ü |

50% |

75% |

ü |

ü*** |

|

Blood (first 3 pints) |

ü |

ü |

ü |

ü |

ü |

ü |

50% |

75% |

ü |

ü |

|

Part A hospice care

coinsurance or copayment |

ü |

ü |

ü |

ü |

ü |

ü |

50% |

75% |

ü |

ü |

|

Skilled nursing

facility care coinsurance |

X |

X |

ü |

ü |

ü |

ü |

50% |

75% |

ü |

ü |

|

Part A deductible |

X |

ü |

ü |

ü |

ü |

ü |

50% |

75% |

50% |

ü |

|

Part B deductible |

X |

X |

ü |

X |

ü |

X |

X |

X |

X |

X |

|

Part B excess charge |

X |

X |

X |

X |

ü |

ü |

X |

X |

X |

X |

|

Foreign travel

exchange (up to plan limits) |

X |

X |

80% |

80% |

80% |

80% |

X |

X |

80% |

80% |

|

Out-of-pocket limit** |

N/A |

N/A |

N/A |

N/A |

N/A |

N/A |

$6,940 in 2023

($7,060 in 2024) |

$3,470 in 2023

($3,530 in 2024) |

N/A |

N/A |

|

Premium Cost (example of male, age 65, living in the Northern VA

area) |

$77 - $1,292 |

$123 - $352 |

$178 - $440 |

$138 - $241 |

$141 - $443 |

$119 - $419 |

$59 - $147 |

$80 - $247 |

$131 - $379 |

$93 - $359 |

*Plans F & G offer a high deductible plan in some states.

**Plans K & L show how much they’ll pay for approved services before you meet your out-of-pocket yearly limit and Part B deductible. After you meet them, the plan will pay 100% for approved services.

***Plan N pays 100% of the costs of Part B services, except for copayments for some office visits and some emergency room visits.

What is covered with Medigap?

Medigap policies help cover out-of-pocket costs associated with Original Medicare, like:

- Copayments

- Coinsurance

- Deductibles

Some Medigap policies cover services that Original Medicare doesn’t cover, like emergency medical care when you travel outside the U.S. (foreign travel emergency care).

What is NOT covered?

- Long-term care (like in a nursing home)

- Vision or dental care

- Hearing aids

- Eyeglasses

- Private-duty nursing

Medigap Costs

Medigap premiums vary depending on the insurance company, the plan, and where you live. The benefits in each lettered plan are the same, no matter which insurance company sells it. The premium amount is the only difference between policies with the same plan letter sold by different companies. There can be big differences in the premiums that different insurance companies charge for the same coverage, so be sure you compare Medigap plans with the same letter (for example, compare Plan G from one company with Plan G from another company).

Medigap Open Enrollment Period

Under federal law, you get a 6 month “Medigap Open Enrollment” period. It starts the first month you have Medicare Part B and you’re 65 or older. During this time, you:

- Can enroll in any Medigap policy.

- Will generally get better prices and more choices among policies.

- You can buy any Medigap policy sold in your state. An insurance company can’t use medical underwriting to decide whether to accept your application – they can’t deny you coverage due to pre-existing health problems.

- Can avoid or shorten waiting periods for a pre-existing condition if you buy a Medigap policy to replace “creditable coverage.”

What if I miss my Medigap Open Enrollment Period?

- You may have to pay more for a policy.

- Fewer policy options may be available to you.

- The insurance company is allowed to deny you a policy if you don’t meet their medical underwriting requirements.

Can you switch between Medicare Advantage (Part C) and Medigap?

Yes, possibly with restrictions such as higher premiums and medical underwriting. There are multiple steps to switch to Medigap.

- Drop your Medicare Advantage

- Return to Original Medicare

- Apply for Medigap

Unless you meet the following you will have to wait until certain times of the year.

- Moving outside of your current plan’s service area

- Your plan ending, ceasing to serve the area where you live or significantly reducing its provider network

- Qualifying for assistance from the Medicare Extra Help program

Enrollment periods include:

- The Medicare Advantage Open Enrollment Period (OEP) between January 1 and March 31

- The Annual Election Period (AEP), between October 15 and December 7

Important Note! In most cases, when you switch from Medicare Advantage to Original Medicare, you lose your “guaranteed-issue” rights for Medigap. You generally have guaranteed-issue rights for six months when you are both 65 or older and enrolled in Medicare Part B. Guaranteed-issue rights ensure that you can buy any plan sold in your state, and will not be charged a higher premium based on your health status. If the insurance company finds you are too high of a risk it can refuse to insure you or may charge a much higher premium.

Medicare Advantage vs Medicare Supplement Comparison

|

Plan Features |

Medicare Advantage |

Medicare Supplement |

|

Coverage |

Original Medicare Parts A and B and additional coverage:

dental, vision, hearing, and fitness services |

Also known as Medigap, fills the gap in coverage that

creates out-of-pocket costs from Parts A and B. |

|

Enrollment |

There are specific enrollment periods during the year

when you can enroll in or switch to a different Medicare Advantage plan |

You can apply to buy a Medigap plan any time after you

turn 65 and join Part B (may be required to take physical) |

|

Doctors and Hospitals |

May be required to use in-network doctors and hospitals |

Not required to see in-network doctors. May see any

doctor nationwide that accepts Medicare |

|

Referrals |

May need a referral for a specialist |

No referrals required |

|

Costs |

Lower premiums - may have copays |

Higher premiums – smaller copays or none |

|

Prescription Drug Coverage |

Most of the time included with the plan |

Not included, will need to pick up Part D |

|

Medical Underwriting |

None |

Yes, unless you enroll during your initial enrollment

period (starts 3 months before the month you turn age 65, and ends 3 months

after) |

Special Enrollment Period

Original Medicare (Part B)

For a more detailed explanation on the SEP for Medicare Part B you can find our article Navigating Medicare: Understanding Special Enrollment Periods (SEP) for Part B

Normally, Medicare enrollment starts 3 months before the month you turn age 65 and 3 months after. You are required to sign up for Medicare during this time. However, there are situations where you may have other coverage already in place or be unable to enroll due to circumstances beyond your control. Instead of applying the penalty, the Medicare program allows an exception process so you can still enroll. This process is referred to as the Medicare Special Enrollment Period or SEP.

Medicare Advantage (Part C) & Medigap

- Moving outside of your current plan’s service area

- Your plan ending, ceasing to serve the area where you live or significantly reducing its provider network

- Qualifying for assistance from the Medicare Extra Help program

Medicare Advantage

Medicare Advantage Open Enrollment Period – January 1 to March 31

Have a Medicare Advantage plan? Then during the annual Medicare Advantage Open Enrollment Period, you can:

- Switch to a different Medicare Advantage plan.

- Drop your Medicare Advantage plan and go back to Original Medicare. You can then choose to join a standalone Part D plan.

Annual Enrollment Period (AEP) – October 15 to December 7

Each year during the AEP, you can make changes to your Medicare coverage for the following year. You can:

- Switch to a different Medicare Advantage, Medicare Cost or standalone Part D plan.

- Enroll in a Medicare Advantage, Medicare Cost or standalone Part D plan for the first time.

- Drop your Medicare Advantage, Medicare Cost or standalone Part D plan and go back to Original Medicare. You can then choose to apply for a Medicare Supplement plan.

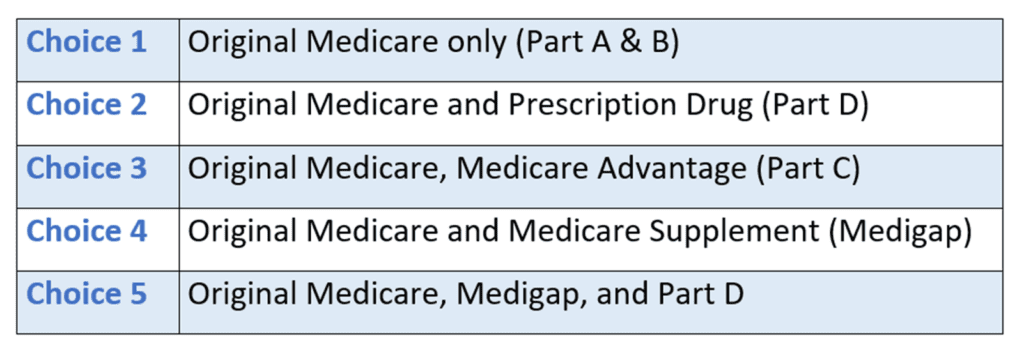

Summary of choices available

Reach Out to Us!

If you have additional federal benefit questions, reach out to our team of CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Federal Employee Benefits Consultants (ChFEBC℠), and Accredited Investment Fiduciaries (AIF®). At PlanWell, we focus on retirement planning for federal employees. Learn more about our process designed for the career federal employee.

Preparing for a federal retirement? Check out our scheduled federal retirement workshops. Sign up for our no-cost federal retirement webinars here! Make sure to plan ahead and reserve your seat for our FERS webinar, held every three weeks. Interested in having PlanWell host a federal retirement seminar for your agency? Reach out, and we can collaborate with HR to arrange an on-site FERS seminar.

Want to fast-track your federal retirement plan? Skip the FERS webinar and start a one-on-one conversation with a ChFEBC today. You can schedule a one-on-one meeting here.

About Brennan Rhule

Co-Founder & Financial Planner · CFP®, ChFEBC℠, AIF®

Brennan graduated from Virginia Tech's CFP Board-Registered program and has spent over 15 years in the Washington, DC area working with federal employees. His experience led him to earn the ChFEBC℠ designation—becoming a true specialist in federal benefits. Brennan's mission is simple: cut through the complexity. Federal retirement rules can feel overwhelming, but with the right guidance, every employee can retire with confidence. He loves seeing the weight lift off clients' shoulders when they finally have a clear plan.